Retail vs. Foodservice: The Battle for the Consumer’s Wallet

- Amaury Marescaux

- Apr 21

- 2 min read

INSIGHT - The Belgian consumer has never been so solicited. And never have they been so free to choose where they spend their food euro. Mass retail and out-of-home dining are engaged in a true duel: who captures what, when, and at what price?

The duel. On one side, mass retail is extending its hours, developing its catering offers, and installing food corners at the front of its aisles. On the other side, a foodservice sector seeks to capture consumption occasions that retail is methodically nibbling away at. Between the two, a consumer arbitrates in real-time, depending on the occasion, the time, and their level of hunger.

This war of channels has intensified considerably. As we noted in our analysis of supermarkets open on Sundays, the redefining of opening hours has opened an additional front on a terrain that foodservice believed was secure. Today, the question is no longer framed in terms of channel, but in terms of occasion: who captures what, when, and at what price?

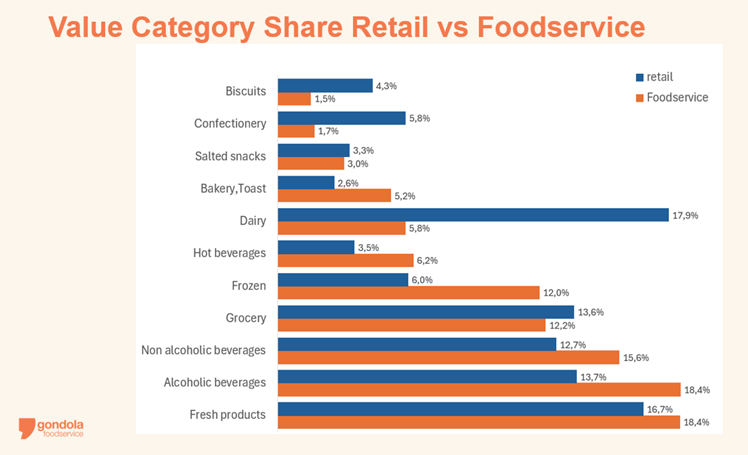

Categories reveal two different DNAs, and that is where the stakes begin

The data from the GFS Cube allows for this battle to be quantified. The composition of purchases by channel reveals structural imbalances that are not merely descriptive: they indicate where each channel naturally holds the upper hand, and where it is vulnerable.

Dairy illustrates the case of retail dominating without possible contestation: 17.9% of retail value versus 5.8% in foodservice, which is a 12-point difference. No restaurant, which captures 58% of foodservice value, serves a yogurt or a glass of milk at the table. The cheese category, however, is well-represented in fast food. The same logic applies to confectionery and biscuits, which are over-represented in retail. This is true even if dairy catches up in institutional catering, and confectionery and biscuits in convenience stores, accounting for 10% of foodservice value.

Conversely, alcoholic beverages account for 18.4% of foodservice value compared to 13.7% in retail (+4.7 percentage points). Non-alcoholic beverages show a +2.9 percentage point difference on the foodservice side. The entire social and experiential dimension of out-of-home consumption is captured there. Furthermore, frozen food accounts for 12.0% in foodservice versus 6.0% in retail, remaining true to the DNA of professional kitchens: standardization, cost management, and volumes. It is a category structurally linked to the professional channel, invisible on the consumer’s plate, but central to the economic equation of the operator.

For a manufacturer or a wholesaler, reading these gaps is not an academic exercise. It is a go-to-market signal. A category that outperforms in foodservice deserves a commercial strategy dedicated to the channel, an adapted format, and a different service logic. A category that is less represented in foodservice, such as confectionery (1.7%), must analyze the channels where new opportunities are emerging and the possibilities for cross-selling with categories that are performing well.