Between Indifference and Impulse: The Reality and Potential of Food in Service Stations

- Amaury Marescaux

- Apr 14

- 3 min read

INSIGHT - Who stops at the station shop, and to buy what? Behind limited footfall, Food & Beverage (F&B) in service stations reveals contrasting dynamics but also a major potential for transformation in the era of new habits.

For decades, the service station lived by the rhythm of refueling. But these locations are no longer just "gas pump parks"; they could well become new destinations for convenience and premium snacking. This is because, on the road, Belgians are adopting new consumption habits. It is a market in full mutation, where a product's brand does not always trigger the stop, but often secures the sale. The service station sector can no longer settle for a uniform offering. Pioneers have already understood this.

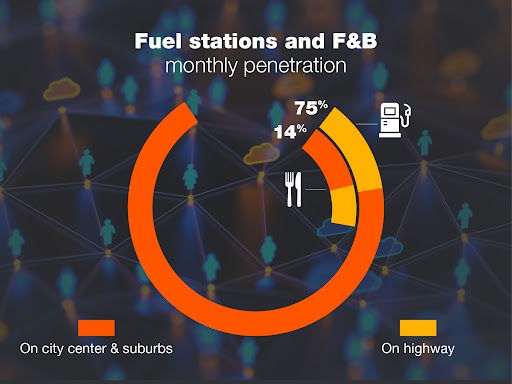

It is best to know the reality on the ground, starting with an unvarnished assessment: F&B footfall in Belgian service station shops remains marginal. According to our Fullmoon data model, only 13.8% of consumers shop there more than once a month. This penetration drops even further among certain profiles: it falls to 11% among 25-34 and 55-65 year-olds, and remains structurally lower among women across all age groups.

Unsurprisingly, men aged 35-44 constitute the core target for these points of sale, representing 1.5 million potential shoppers. This dominant profile directly influences the brands that make the trip worthwhile.

Among men, the winning combo is unequivocal: Burger King and Coca-Cola appeal to 7 out of 10 men. Women respond more to Panos and Starbucks, two brands that focus on comfort and perceived quality rather than speed.

It should be noted that a group of die-hard motorists remains: 1 in 4 consumers states that no brand would make them stop—a signal that reminds us the battle for attraction remains wide open. However, men and women agree on two impulse staples: Haribo and Lay’s, which are popular in both camps.

An interesting paradox: Jupiler and Red Bull hardly factor into the decision to stop, and even less so for women. However, they are by far the two most purchased categories once inside the store.

Beer and energy drinks rely heavily on impulse. There is, however, an important nuance: beer is in sharp decline (-4.4%), a sign of the category losing steam in stations, while energy drinks grew by +7.4% between 2024 and 2025.

At a Crossroads

The service station is at a crossroads. With 1,400 stores in Belgium, or 1.2 points of sale per 10,000 inhabitants, the network is dense. But the upcoming transformation is considerable. Electric charging profoundly changes the equation: fewer stops, but much longer dwell times, an unprecedented window of opportunity to rethink the shopping experience.

The station of tomorrow looks more like a next-generation convenience store than a simple pit stop between two fill-ups. Some operators have already made the turn: Bruno Corners or G&V, with its Break Point Food Station in Diegem and Waregem, show that a different ambition is possible.

Obviously, the transformation cannot follow a single path.

On the highway, where 65% of F&B purchases are concentrated, the challenge is to offer a consistent range for planned and longer stops: quality catering, expanded choices, and reassuring brands.

In the city, the logic is entirely different: visits are more spontaneous, the customer base is more diverse, and the offering must align with new urban habits: practicality, health, and premium snacking.

Two contexts, two strategies. Operators who understand this will gain a competitive head start.